Currently, mortgage rates are close to double what they were a year ago.

Why have those rates gone up so much? When the Fed wants to tighten the money supply, its policies typically result in increased interest rates on consumer borrowing (which includes mortgage rates). It’s all part of the Federal Reserve’s attempt to curb inflation which is currently the highest it’s been in four decades.

Those high rates, paired with historically high home prices, are leaving many potential home buyers wondering if they should wait to begin their home search. Current homeowners also face a dilemma: despite the opportunity to cash in on surging equity appreciation, they find themselves inclined to hold on to the low mortgage rate they locked in years ago instead of selling their current dwelling and upgrading to something new where they risk having a higher monthly payment.

How is this dynamic affecting the overall real estate market?

According to a recent Realtor.com forecast, home price growth is expected to cool nationwide, but since it’s remained hotter longer, by fall 2022 buying activity will still hit a 15-year high, second only to the buying activity of 2021.

Danielle Hale, the chief economist at Realtor.com says it’s important to consider what’s happening in the specific region you’re looking to buy or sell in. “The local area where you’re trying to buy could be more or less buyer-friendly than the national data indicates.” This is why we must track the numbers here in Raleigh, rather than rely on national headlines.

Around the country, certain very hot markets are cooling faster than others. For instance, a new Redfin analysis shows that many markets on the West Coast (northern California and Washington) are cooling the fastest. In looking at a variety of data points ranging from home value appreciation, to employment numbers, to job growth, and cost of living, we can assess how North Carolina is doing in comparison. The findings are heartening, confirming that our state is a quality place to live with a housing market that projects a great deal of strength and stability moving forward.

How do things look in Raleigh?

With its strong housing appreciation, steady job growth, and promising cost-of-living ranking, North Carolina is #7 in the nation on Bankrate.com’s housing heat index. Clearly, the state has a lot going for it. In July 2022, CNBC put North Carolina at #1 on its list of Top States for Business, also noting that North Carolina ranked #1 in the Economy category of their survey which factors in the health of the state’s housing market.

This map from Freddie Mac shows that North Carolina has received a great deal of positive pre- and post-pandemic net migration due to these factors.

In fact, PricewaterhouseCoopers named Raleigh, which it described as a magnet supernova city, the #1 city in the U.S. for homebuilding prospects in their 2022 Emerging Trends in Real Estate Study. PwC also rated the city number two in the nation for overall real estate prospects, and found that in 2022 Raleigh houses spent half the time on the market then they did in 2021.

Multiple experts seem to agree: Raleigh’s current trajectory indicates economic growth.

And in the current economic environment, where inflation is projected to continue, living in Raleigh is a smart choice as the median amount spent on housing in Raleigh is 15.6% of an individual’s income as opposed to the ultra-high 30% national average. Looking for a good place to ride out inflation? Raleigh is where you want to be.

What are some market factors to keep an eye on in the future?

Price reductions are a powerful leading indicator related to the current, active market. It’s an indicator that we all need to take a closer look at. In a normal market, about a third of the listings take a price cut according to data from Altos Research. But in the beginning of 2022, price cuts were rare. Now that we’re seeing them again, they indicate a shift taking place in the market, though, contrary to what many click-bait headlines will have you believe, they don’t necessarily mean the overall rate of home value appreciation is coming down.

Let’s parse out the data and what it means:

In June 2022, 25.9% of homes listed for sale in Raleigh experienced a price drop. This compares with 5.5% in June of 2021. That may seem like a lot, but keep in mind what the typical percentage of listed home price reductions is—about 30%. In fact, if you look at 2018, price drops peaked at 37.2%. Again, we’re nowhere near there. What appears to be happening is a cooling of the rate of price acceleration, but prices still appear to be increasing year over year as long as inventory remains low. In fact, according to Realtor.com, homes in Raleigh sold for 1.64% above the asking price in June 2022.

So, what’s happening with inventory?

The average national inventory since about 2000 has been 2.335 million existing homes listed. Currently, we are at 1.03 million. So, nationally, the market would need to more than double its inventory to get back to normal. Some factors preventing that increase in inventory include the constraints on new home building caused by supply chain issues, the large percentage of institutions that have bought up homes and kept them off the market (either to use as investment income or highly-priced rental units), and the current high mortgage rates which dissuade homeowners from giving up the low rates they’ve locked in when they bought their properties years ago. All these factors are keeping the local and national housing inventory from rising back to the normal level, and so prices will continue to remain high.

And inventory in Raleigh, specifically?

https://media.agentaprd.com/sites/169/chart.webp?quality=80 1x, https://media.curaytor.com/resize-1408-0/f5dcef56-9dda-427e-a630-d373551c8122/img.webp?quality=80 2x”>

Where is inventory projected to go in the future?

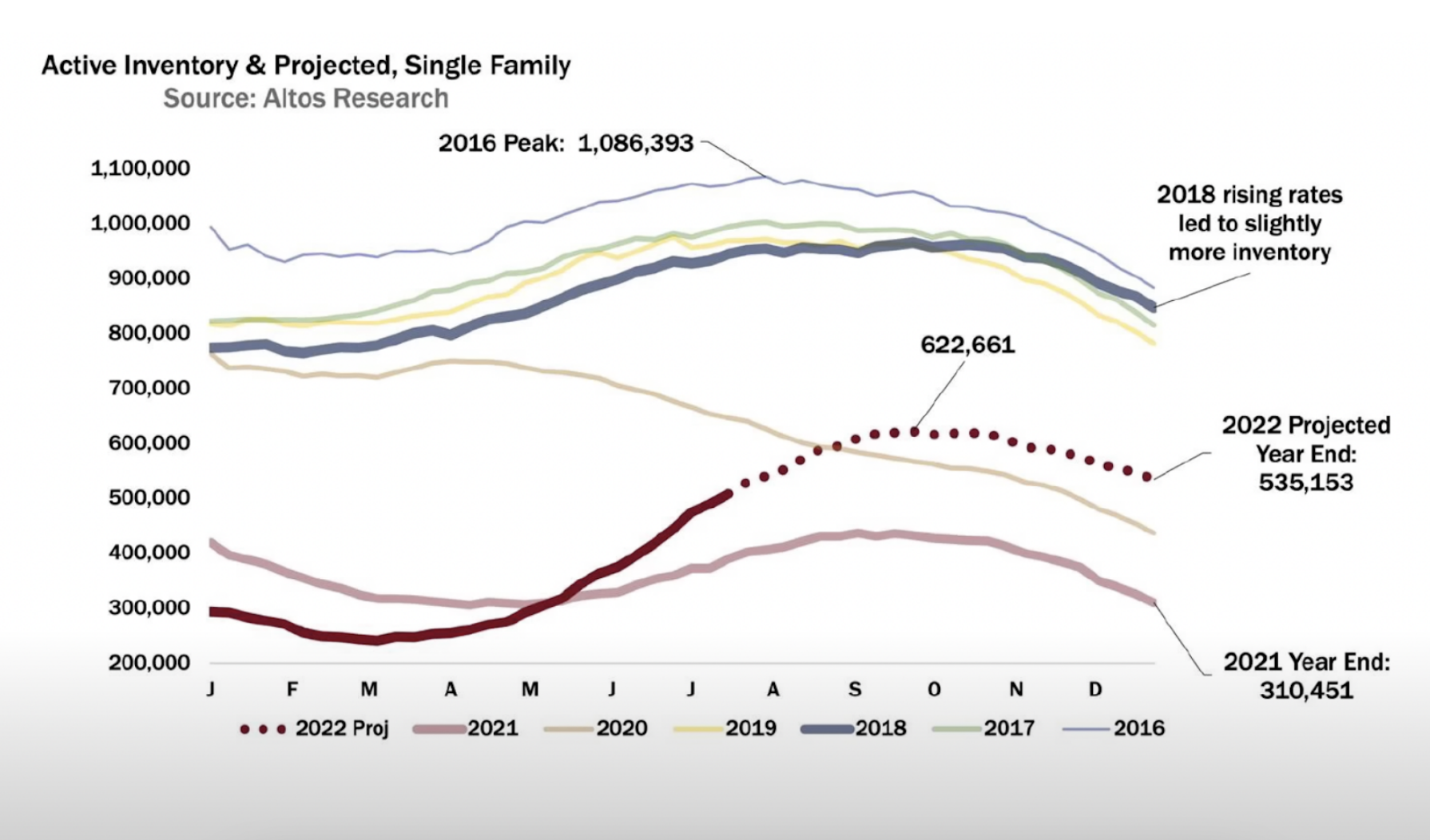

Data from Altos Research shows that total inventory of homes for sale in the U.S. rose to 508,716 in July 2022. That’s the most the country has had in almost 2 years. 31% more than last year at this time. Altos’ CEO Mike Simonsen expects “a few more weeks of hefty increases in inventory this summer,” ultimately projecting that nationwide inventory will peak between September and October with an estimated 622,661 homes on the market, ending the year at 535,153. Still, about 200-400,000 below typical pre-pandemic levels recorded in 2016-2019.

Raleigh, in fact, was one of the top inventory gainers, increasing 111.7% year over year, and, according to Realtor.com, we’ve experienced a 37% increase in new listings from June to July 2022. This is good news for buyers who’ve been finding themselves outbid in the Raleigh market. They now face less competition and are, at last, able to snag a home.

But we need to consider the impact of a pricey monthly payment on those already feeling the pain of high inflation. Due to high mortgage rates as well as the inflationary increase in the cost of living, that monthly payment can seem unmanageable. For many, that means making the choice to rent for a longer period of time before looking into home ownership, choosing a home that’s smaller or possibly even a fixer-upper, or making sacrifices in other areas of life to make the monthly housing payment work.

https://media.agentaprd.com/sites/169/chart.webp?quality=80 1x, https://media.curaytor.com/resize-1408-0/8de5cf51-0bf8-47d3-94d0-73337b6a6319/img.webp?quality=80 2x”>

What about those mortgage rates? Are they going down anytime soon?

We’ve rounded up some opinions from different experts to see where they project mortgage rates going in the rest of 2022.

Tabitha Mazzara, director of operations at Mortgage Bank of California says, “If you’re waiting for prices to suddenly plummet to what they were in the past, you’re making a mistake. The Fed has promised another interest rate boost. If you’re ready to buy, don’t wait because prices aren’t headed dramatically downwards to what our parents paid. Things might dip a bit, but there’s no cliff dive that’s going to happen.”

Lawrence Yun, chief economist for the National Association of Realtors echoes that sentiment. “Only when inflation calms down,” he says, “will mortgage rates also begin to stabilize.”

Similarly, Danielle Hale, the chief economist at Realtor.com, projects, “I expect mortgage rates to move toward 5.5% by the end of 2022.”

To get a better understanding of just how serious the inflation situation currently is, let’s take a look at this data from the Bureau of Labor Statistics. As you’https://media.agentaprd.com/sites/169/chart.webp?quality=80 1x, https://media.curaytor.com/resize-1408-0/31f5d3c6-047c-458a-b4b3-e0fe5613584d/img.webp?quality=80 2x”>

If you’re a potential homebuyer eager to get more buying power out of your hard-earned cash you, understandably, might be wondering when inflation will go down. The Fed’s goal is to keep inflation at 2% year-over-year, but with current inflation at 9.1% (did I mention we’re at a 40-year high?) the Fed would need to take drastic measures to reduce that, which is unlikely to happen in an amount significant enough to result in deflation. Recently, Goldman Sach’s CEO Michael Solomon stated that while inflation is expected to “move lower in the second half of the year,” he warned that it’s currently “deeply entrenched” in the U.S. economy. Unlike so-called transitory inflation, entrenched inflation occurs when price increases hit certain categories like rent and health care services that aren’t likely to come down soon.

In summary, it looks like inflation will remain high, mortgage rates will remain high, and home prices will remain high for the foreseeable future. If you’re thinking of buying a home, and your financial circumstances are in a good place for home ownership, it might be smart to do it now. Not only is real estate a good hedge against inflation, but home values are projected to continue rising. T. Rowe Price notes that real estate is among the commodities that historically perform well during inflation cycles.

In Raleigh, this might be especially true as home values have increased 34.7% over the past year.

Additionally, the economists at Freddie Mac project nationwide home price growth to level off but continue in a positive direction, projecting a 5% home price growth in 2023.

It seems near-term relief from inflation and high mortgage rates is unlikely. What’s the best move?

If you’re currently renting and aren’t living in a region protected by rent control laws, you’ve probably seen your monthly payment increase. Nationally, rents have increased over 14% this year. That’s a lot of money going to pay someone else’s mortgage.

While high mortgage rates certainly make many folks question the affordability of homeownership, if you’re planning on the home you buy to be your “forever” home—and if you can make the monthly payment work by choosing a smaller house, one in a less-expensive location, or by reducing your personal expenses in other ways—then you might want to step into the market and see what’s available.

For those thinking of selling, you’ve probably noticed your equity is higher than it’s ever been and you might be eager to cash-in on all this appreciation in value. Some potential sellers, though, may fear taking on a higher mortgage rate than you were previously paying. If you’re looking to downsize your living situation or move to a more economical area, selling now might be a smart move as you could pay for a more modest house using all your accrued equity and possibly forgo a mortgage all together.

Plenty of options are available for both buyers and sellers in the current market. Reach out to our team. We’d love to help you make the moves that are right for your finances.

Schedule a call today!

Give us a call today (828) 818-8894 to discuss your buying or selling your home in Raleigh!

Social Cookies

Social Cookies are used to enable you to share pages and content you find interesting throughout the website through third-party social networking or other websites (including, potentially for advertising purposes related to social networking).